56 Shifts in Aggregate Demand

Laura Prince and OpenStax

Learning Objectives

Type your learning objectives here.

- Explain how imports influence aggregate demand

- Identify ways in which business confidence and consumer confidence can affect aggregate demand

- Explain how government policy can change aggregate demand

- Evaluate why economists disagree on the topic of tax cuts

As we mentioned previously, the components of aggregate demand are consumption spending (C), investment spending (I), government spending (G), and spending on exports (X) minus imports (M). (Read the following Clear It Up feature for explanation of why imports are subtracted from exports and what this means for aggregate demand.) A shift of the AD curve to the right means that at least one of these components increased so that a greater amount of total spending would occur at every price level. A shift of the AD curve to the left means that at least one of these components decreased so that a lesser amount of total spending would occur at every price level. The Keynesian Perspective will discuss the components of aggregate demand and the factors that affect them. Here, the discussion will sketch two broad categories that could cause AD curves to shift: changes in consumer or firm behavior and changes in government tax or spending policy.

Clear It Up

Do imports diminish aggregate demand?

We have seen that the formula for aggregate demand is AD = C + I + G + X – M, where M is the total value of imported goods. Why is there a minus sign in front of imports? Does this mean that more imports will result in a lower level of aggregate demand? The short answer is yes, because aggregate demand is defined as total demand for domestically produced goods and services.

When an American buys a foreign product, for example, it gets counted along with all the other consumption. Thus, the income generated does not go to American producers, but rather to producers in another country. It would be wrong to count this as part of domestic demand. Therefore, imports added in consumption are subtracted back out in the M term of the equation.

Because of the way in which we write the demand equation, it is easy to make the mistake of thinking that imports are bad for the economy. Just keep in mind that every negative number in the M term has a corresponding positive number in the C or I or G term, and they always cancel out.

How Changes by Consumers and Firms Can Affect AD

When consumers feel more confident about the future of the economy, they tend to consume more. If business confidence is high, then firms tend to spend more on investment, believing that the future payoff from that investment will be substantial. Conversely, if consumer or business confidence drops, then consumption and investment spending decline.

The University of Michigan publishes a survey of consumer confidence and constructs an index of consumer confidence each month. The survey results are then reported, which break down the change in consumer confidence among different income levels. According to that index, consumer confidence averaged around 90 prior to the Great Recession, and then it fell to below 60 in late 2008, which was the lowest it had been since 1980. During the 2010s, confidence has climbed from a 2011 low of 55.8 back to a level in the upper 90s, before falling to the lower 70s in 2020 due to the COIVD-19 pandemic, which economists consider close to a healthy state.

The Organization for Economic Development and Cooperation (OECD) publishes one measure of business confidence: the “business tendency surveys”. The OECD collects business opinion survey data for 21 countries on future selling prices and employment, among other business climate elements. After sharply declining during the Great Recession, the measure has risen above zero again and is back to long-term averages (the indicator dips below zero when business outlook is weaker than usual). Of course, either of these survey measures is not very precise. They can however, suggest when confidence is rising or falling, as well as when it is relatively high or low compared to the past.

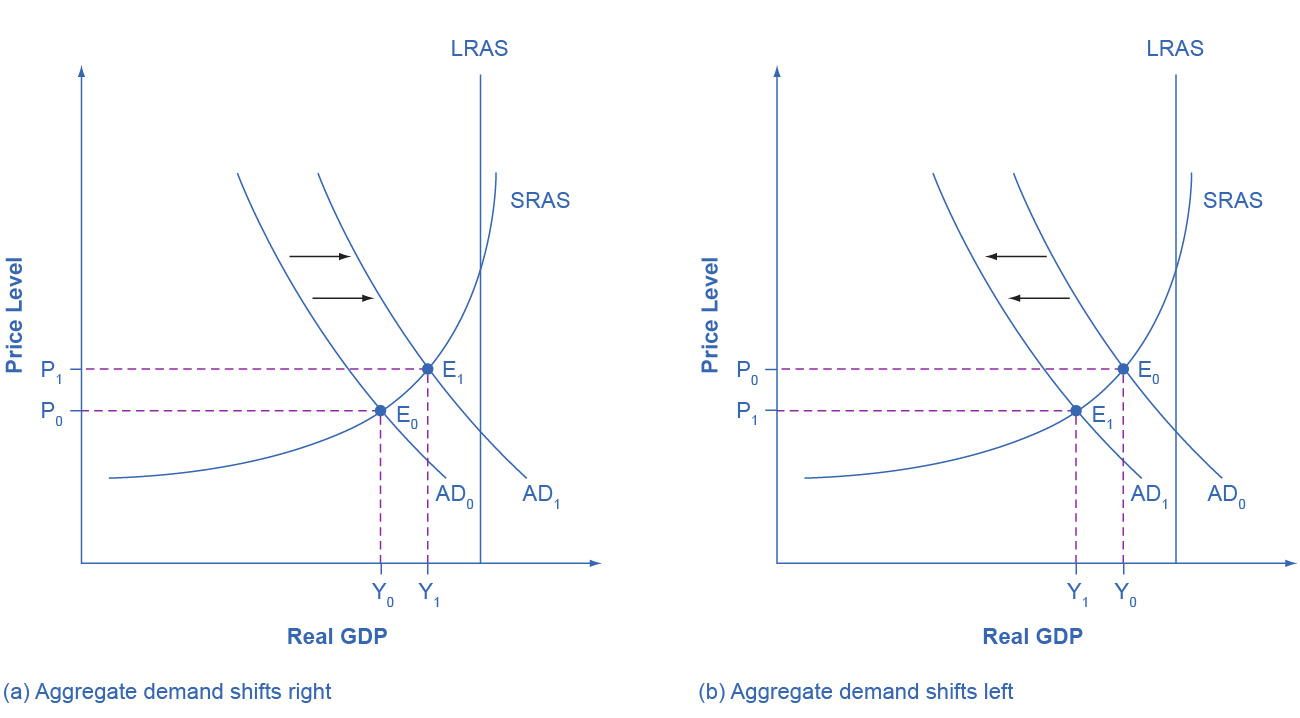

Because economists associate a rise in confidence with higher consumption and investment demand, it will lead to an outward shift in the AD curve, and a move of the equilibrium, from E0 to E1, to a higher quantity of output and a higher price level, as Figure 24.8 (a) shows.

Consumer and business confidence often reflect macroeconomic realities; for example, confidence is usually high when the economy is growing briskly and low during a recession. However, economic confidence can sometimes rise or fall for reasons that do not have a close connection to the immediate economy, like a risk of war, election results, foreign policy events, or a pessimistic prediction about the future by a prominent public figure. U.S. presidents, for example, must be careful in their public pronouncements about the economy. If they offer economic pessimism, they risk provoking a decline in confidence that reduces consumption and investment and shifts AD to the left, and in a self-fulfilling prophecy, contributes to causing the recession that the president warned against in the first place. Figure 24.8 (b) shows a shift of AD to the left, and the corresponding movement of the equilibrium, from E0 to E1, to a lower quantity of output and a lower price level.

Link It Up

Visit this website for data on consumer confidence.

Link It Up

Visit this website for data on business confidence.

Figure 24.8 Shifts in Aggregate Demand (a) An increase in consumer confidence or business confidence can shift AD to the right, from AD0 to AD1. When AD shifts to the right, the new equilibrium (E1) will have a higher quantity of output and also a higher price level compared with the original equilibrium (E0). In this example, the new equilibrium (E1) is also closer to potential GDP. An increase in government spending or a cut in taxes that leads to a rise in consumer spending can also shift AD to the right. (b) A decrease in consumer confidence or business confidence can shift AD to the left, from AD0 to AD1. When AD shifts to the left, the new equilibrium (E1) will have a lower quantity of output and also a lower price level compared with the original equilibrium (E0). In this example, the new equilibrium (E1) is also farther below potential GDP. A decrease in government spending or higher taxes that leads to a fall in consumer spending can also shift AD to the left.

How Government Macroeconomic Policy Choices Can Shift AD

Government spending is one component of AD. Thus, higher government spending will cause AD to shift to the right, as in Figure 24.8 (a), while lower government spending will cause AD to shift to the left, as in Figure 24.8 (b). For example, in the United States, government spending declined by 3.2% of GDP during the 1990s, from 21% of GDP in 1991, and to 17.8% of GDP in 1998. However, from 2005 to 2009, the peak of the Great Recession, government spending increased from 19% of GDP to 21.4% of GDP. If changes of a few percentage points of GDP seem small to you, remember that since GDP was about $14.4 trillion in 2009, a seemingly small change of 2% of GDP is equal to close to $300 billion. Since 2009, government expenditures have gone back down to around 17–18% of GDP, although in 2020 they rose to 18.5%.

Tax policy can affect consumption and investment spending, too. Tax cuts for individuals will tend to increase consumption demand, while tax increases will tend to diminish it. Tax policy can also pump up investment demand by offering lower tax rates for corporations or tax reductions that benefit specific kinds of investment. Shifting C or I will shift the AD curve as a whole.

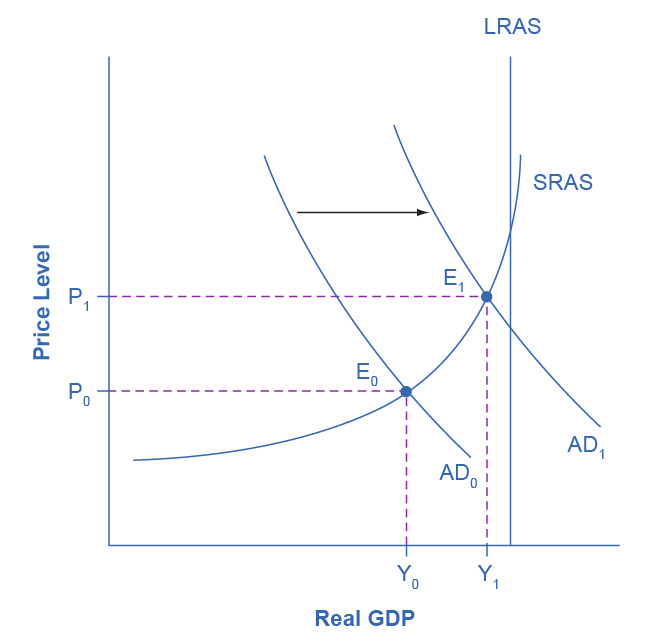

During a recession, when unemployment is high and many businesses are suffering low profits or even losses, the U.S. Congress often passes tax cuts. During the 2001 recession, for example, the U.S. Congress enacted a tax cut into law. At such times, the political rhetoric often focuses on how people experiencing hard times need relief from taxes. The aggregate supply and aggregate demand framework, however, offers a complementary rationale, as Figure 24.9 illustrates. The original equilibrium during a recession is at point E0, relatively far from the full employment level of output. The tax cut, by increasing consumption, shifts the AD curve to the right. At the new equilibrium (E1), real GDP rises and unemployment falls and, because in this diagram the economy has not yet reached its potential or full employment level of GDP, any rise in the price level remains muted. Read the following Clear It Up feature to consider the question of whether economists favor tax cuts or oppose them.

Figure 24.9 Recession and Full Employment in the AD/AS Model Whether the economy is in a recession is illustrated in the AD/AS model by how close the equilibrium is to the potential GDP line as indicated by the vertical LRAS line. In this example, the level of output Y0 at the equilibrium E0 is relatively far from the potential GDP line, so it can represent an economy in recession, well below the full employment level of GDP. In contrast, the level of output Y1 at the equilibrium E1 is relatively close to potential GDP, and so it would represent an economy with a lower unemployment rate.

Clear It Up

Do economists favor tax cuts or oppose them?

One of the most fundamental divisions in American politics over the last few decades has been between those who believe that the government should cut taxes substantially and those who disagree. Ronald Reagan rode into the presidency in 1980 partly because of his promise, soon carried out, to enact a substantial tax cut. George Bush lost his bid for reelection against Bill Clinton in 1992 partly because he had broken his 1988 promise: “Read my lips! No new taxes!” In the 2000 presidential election, both George W. Bush and Al Gore advocated substantial tax cuts and Bush succeeded in pushing a tax cut package through Congress early in 2001. More recently in 2017 and 2018, Donald Trump initiated a new round of tax cuts throughout the economy, and President Biden promised his own set of tax cuts in his 2021 spending bills.

What side do economists take? Do they support broad tax cuts or oppose them? The answer, unsatisfying to zealots on both sides, is that it depends. One issue is whether equally large government spending cuts accompany the tax cuts. Economists differ, as does any broad cross-section of the public, on how large government spending should be and what programs the government might cut back. A second issue, more relevant to the discussion in this chapter, concerns how close the economy is to the full employment output level. In a recession, when the AD and AS curves intersect far below the full employment level, tax cuts can make sense as a way of shifting AD to the right. However, when the economy is already performing extremely well, tax cuts may shift AD so far to the right as to generate inflationary pressures, with little gain to GDP.

With the AD/AS framework in mind, many economists might readily believe that the 1981 Reagan tax cuts, which took effect just after two serious recessions, were beneficial economic policy. Similarly, Congress enacted the 2001 Bush tax cuts and the 2009 Obama tax cuts during recessions. However, some of the same economists who favor tax cuts during recession would be much more dubious about identical tax cuts at a time the economy is performing well and cyclical unemployment is low.

Government spending and tax rate changes can be useful tools to affect aggregate demand. We will discuss these in greater detail in the Government Budgets and Fiscal Policy chapter and The Impacts of Government Borrowing. Other policy tools can shift the aggregate demand curve as well. For example, as we will discuss in the Monetary Policy and Bank Regulation chapter, the Federal Reserve can affect interest rates and credit availability. Higher interest rates tend to discourage borrowing and thus reduce both household spending on big-ticket items like houses and cars and investment spending by business. Conversely, lower interest rates will stimulate consumption and investment demand. Interest rates can also affect exchange rates, which in turn will have effects on the export and import components of aggregate demand.

Clarifying the details of these alternative policies and how they affect the components of aggregate demand can wait for The Keynesian Perspective chapter. Here, the key lesson is that a shift of the aggregate demand curve to the right leads to a greater real GDP and to upward pressure on the price level. Conversely, a shift of aggregate demand to the left leads to a lower real GDP and a lower price level. Whether these changes in output and price level are relatively large or relatively small, and how the change in equilibrium relates to potential GDP, depends on whether the shift in the AD curve is happening in the AS curve’s relatively flat or relatively steep portion.

Access for free at https://openstax.org/books/principles-economics-3e