96 The Federal Reserve Banking System and Central Banks

The Federal Reserve Banking System and Central Banks

Learning Objectives

By the end of this section, you will be able to:

- Explain the structure and organization of the U.S. Federal Reserve

- Discuss how central banks impact monetary policy, promote financial stability, and provide banking services

Structure of Macroeconomics

Definition/Goals of Macroeconomics: relatively low unemployment (measured by looking at unemployment rate), relatively stable price (measured by looking at CPI and Inflation rates), economics growth (measured by looking GDP)

Goals are accomplished by using the tools of Monetary and Fiscal Policies.

Monetary Policy are the actions that the Federal Reserve takes to ensure relatively low unemployment, stable prices and growth of economy.

In making decisions about the money supply, a central bank decides whether to raise or lower interest rates and, in this way, to influence macroeconomic policy, whose goal is low unemployment and low inflation. The central bank is also responsible for regulating all or part of the nation’s banking system to protect bank depositors and insure the health of the bank’s balance sheet.

Central Bank (Federal Reserve)

We call the organization responsible for conducting monetary policy and ensuring that a nation’s financial system operates smoothly the central bank. Most nations have central banks or currency boards. Some prominent central banks around the world include the European Central Bank, the Bank of Japan, and the Bank of England. In the United States, we call the central bank the Federal Reserve—often abbreviated as just “the Fed.” This section explains the U.S. Federal Reserve’s organization and identifies the major central bank’s responsibilities.

Structure/Organization of the Federal Reserve

The Federal Reserve is semi-decentralized, mixing government appointees with representation from private-sector banks. At the national level, it is run by a Board of Governors, consisting of seven members appointed by the President of the United States and confirmed by the Senate. Appointments are for 14-year terms and they are arranged so that one term expires January 31 of every even-numbered year. The purpose of the long and staggered terms is to insulate the Board of Governors as much as possible from political pressure so that governors can make policy decisions based only on their economic merits. Additionally, except when filling an unfinished term, each member only serves one term, further insulating decision-making from politics. The Fed’s policy decisions do not require congressional approval, and the President cannot ask for a Federal Reserve Governor to resign as the President can with cabinet positions.

One member of the Board of Governors is designated as the Chair. The current Chair is Jerome Powell. See https://www.federalreserve.gov/aboutthefed/structure-federal-reserve-system.htm

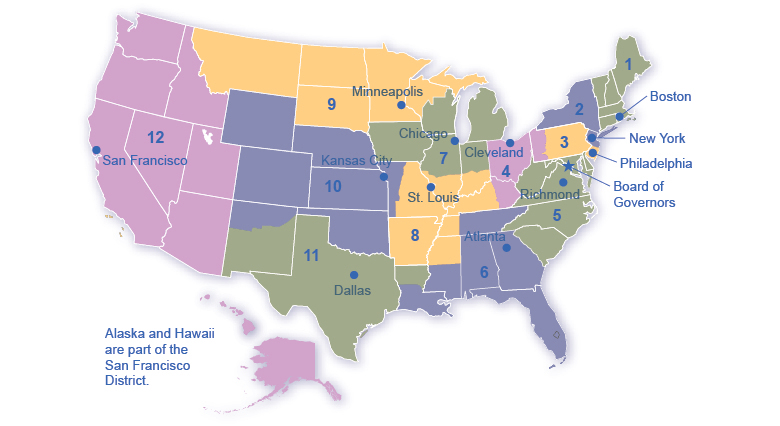

The Federal Reserve is more than the Board of Governors. The Fed also includes 12 regional Federal Reserve banks, each of which is responsible for supporting the commercial banks and economy generally in its district. Figure 28.3 shows the Federal Reserve districts and the cities where their regional headquarters are located. The commercial banks in each district elect a Board of Directors for each regional Federal Reserve bank, and that board chooses a president for each regional Federal Reserve district. Thus, the Federal Reserve System includes both federally and private-sector appointed leaders.

Figure 28.3 The Twelve Federal Reserve Districts There are twelve regional Federal Reserve banks, each with its district.

What Does a Central Bank Do?

The Federal Reserve, like most central banks, is designed to perform three important functions:

- To conduct monetary policy (see section)

- To promote stability of the financial system (see section)

- To provide banking services to commercial banks and other depository institutions, and to provide banking services to the federal government. ( see below)

The first two functions are sufficiently important that we will discuss them in their own modules. The third function we will discuss here.

Banking Services to Banks

The Federal Reserve provides many of the same services to banks as banks provide to their customers. For example, all commercial banks have an account at the Fed where they deposit reserves. Similarly, banks can obtain loans from the Fed through the “discount window” facility, which we will discuss in more detail later. The Fed is also responsible for check processing. When you write a check, for example, to buy groceries, the grocery store deposits the check in its bank account. Then, the grocery store’s bank returns the physical check (or an image of that actual check) to your bank, after which it transfers funds from your bank account to the grocery store’s account. The Fed is responsible for each of these actions.

On a more mundane level, the Federal Reserve ensures that enough currency and coins are circulating through the financial system to meet public demands. For example, each year the Fed increases the amount of currency available in banks around the Christmas shopping season and reduces it again in January.

Finally, the Fed is responsible for assuring that banks are in compliance with a wide variety of consumer protection laws. For example, banks are forbidden from discriminating on the basis of age, race, sex, or marital status. Banks are also required to disclose publicly information about the loans they make for buying houses and how they distribute the loans geographically, as well as by sex and race of the loan applicants.

Access for free at https://openstax.org/books/principles-economics-3e