23 Controlling

Learning Objectives

- How do organizations control activities?

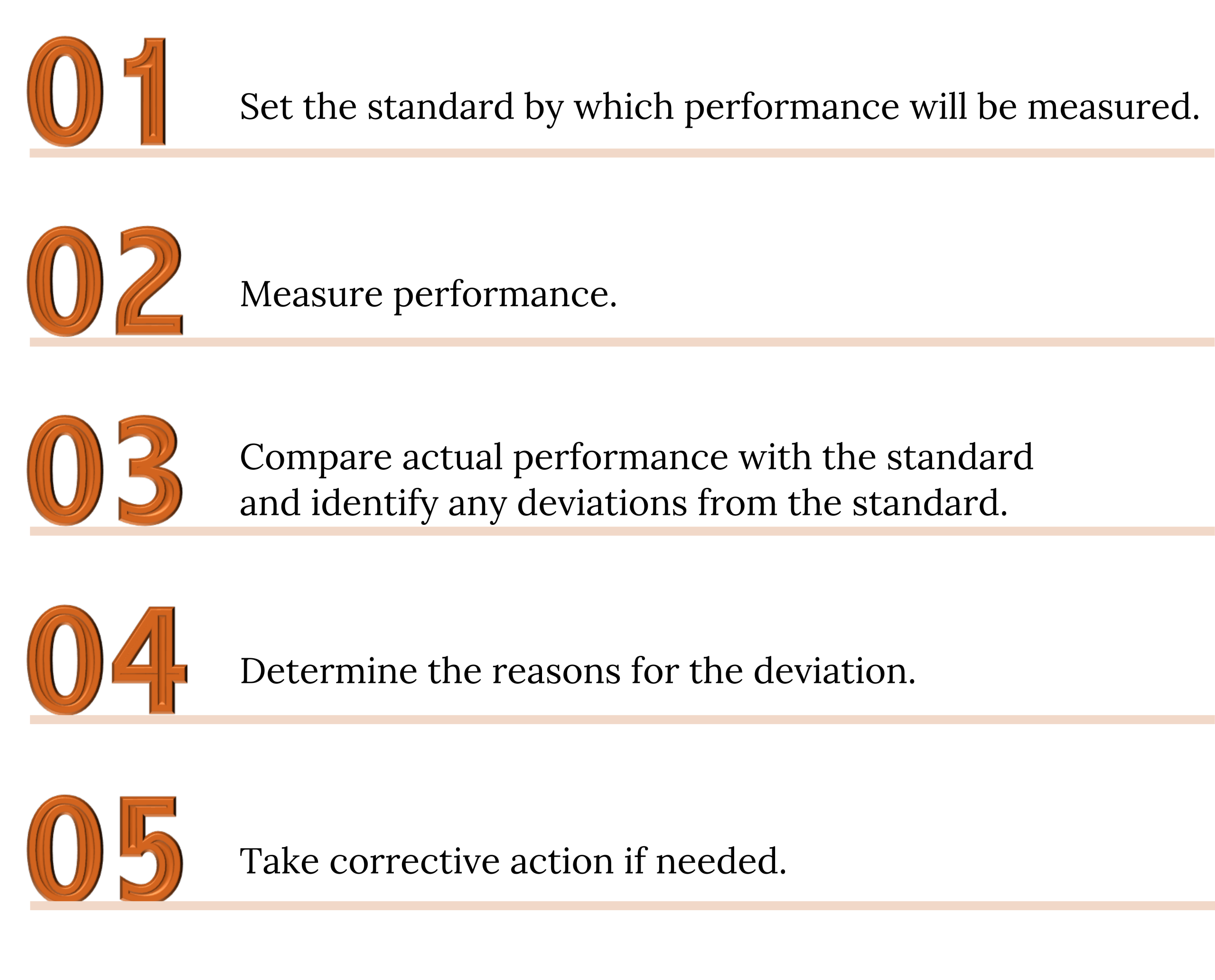

The fourth key function that managers perform is controlling. Controlling is the process of assessing the organization’s progress toward accomplishing its goals. It includes monitoring the implementation of a plan and correcting deviations from that plan. As Exhibit 6.6 shows, controlling can be visualized as a cyclical process made up of five stages:

Performance standards are the levels of performance the company wants to attain. These goals are based on its strategic, tactical, and operational plans. The most effective performance standards state a measurable behavioral objective that can be achieved in a specified time frame. For example, the performance objective for the sales division of a company could be stated as “$200,000 in gross sales for the month of January.” Each individual employee in that division would also have a specified performance goal. Actual firm, division, or individual performance can be measured against desired performance standards to see if a gap exists between the desired level of performance and the actual level of performance. If a performance gap does exist, the reason for it must be determined and corrective action taken.

Feedback is essential to the process of control. Most companies have a reporting system that identifies areas where performance standards are not being met. A feedback system helps managers detect problems before they get out of hand. If a problem exists, the managers take corrective action. Toyota uses a simple but effective control system on its automobile assembly lines. Each worker serves as the customer for the process just before his or hers. Each worker is empowered to act as a quality control inspector. If a part is defective or not installed properly, the next worker won’t accept it. Any worker can alert the supervisor to a problem by tugging on a rope that turns on a warning light (i.e., feedback). If the problem isn’t corrected, the worker can stop the entire assembly line.

Benchmarking

Benchmarking could be considered as a specialized kind of control activity. Rather than controlling a particular aspect of performance (say, defects for a specific product), benchmarking aims to improve a firm’s overall performance. The process of benchmarking involves comparisons to other organizations’ practices and processes with the objective of learning and improvement in both efficiency and effectiveness. Benchmarking exercises can be conducted in a number of ways:

- Organizations often monitor publicly available information to keep tabs on the competition. Annual reports, news articles, and other sources are monitored closely in order to stay aware of the latest developments. In academia, universities often use published rankings tables to see how their programs compare on the basis of standardized test scores, salaries of graduates, and other important dimensions.

- Organizations may also work directly with companies in unrelated industries in order to compare those functions of the business which are similar. A manufacture of aircraft would not likely have a great deal in common with a company making engineered plastics, yet both have common functions such as accounting, finance, information technology, and human resources. Companies can exchange ideas that help each other improve efficiency, and often at a very low cost to either.

- In order to compare more directly to competition without relying solely on publicly available data, companies may enter into benchmarking consortiums in which an outside consultant would collect key data from all participants, anonymize it, and then share the results with all participants. Companies can then gauge how they compare to others in the industry without revealing their own performance to others.

Why is controlling such an important part of a manager’s job? First, it helps managers to determine the success of the other three functions: planning, organizing, and leading. Second, control systems direct employee behavior toward achieving organizational goals. Third, control systems provide a means of coordinating employee activities and integrating resources throughout the organization.

Analyzing Performance

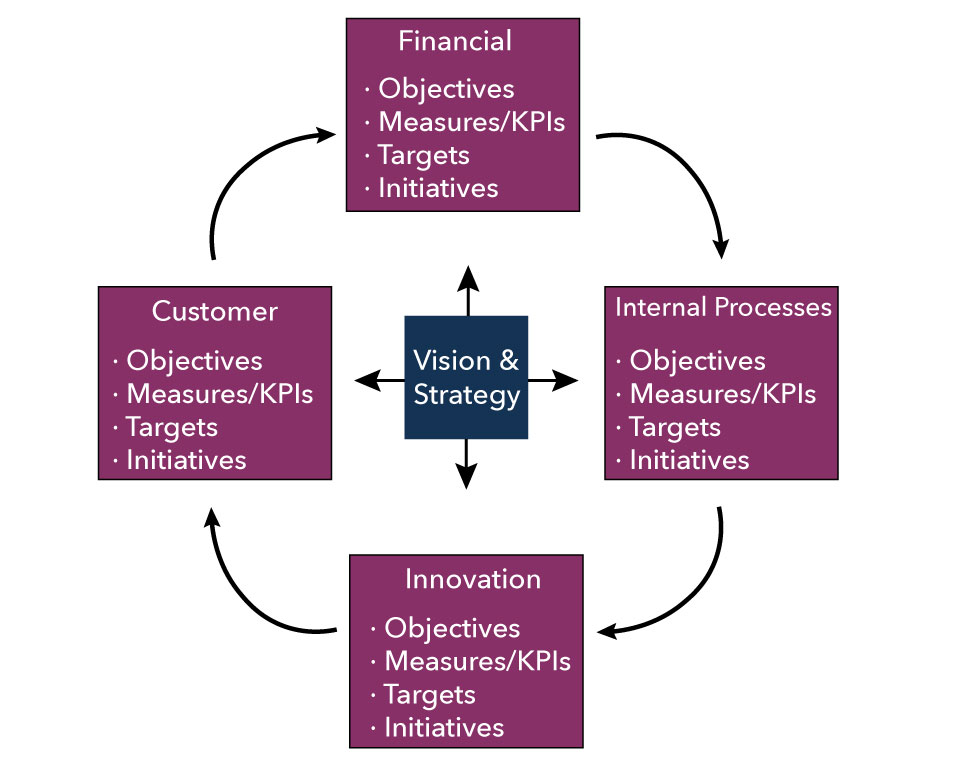

Once performance has been measured, managers must analyze the results and evaluate whether objectives have been met, efficiencies achieved, or goals obtained. The means by which performance is analyzed vary among organizations; however, one tool that has gained widespread adoption is the balanced scorecard. A balanced scorecard is a semi-standardized strategic management tool used to analyze and improve key performance indicators within an organization. The original design of this balanced scorecard has evolved over the last couple decades and now includes a number of other variables—mostly where performance intersects with corporate strategy. Corporate strategic objectives were added to allow for a more comprehensive strategic planning exercise. Today, this second-generation balanced scorecard is often referred to as a “strategy map,” but the conventional “balanced scorecard” is still used to refer to anything consistent with a pictographic strategic management tool.

The following four perspectives are represented in a balanced scorecard:

- Financial: includes measures focused on the question “How do we look to shareholders?”

- Customer: includes measures focused on the question “How do customers perceive us?”

- Internal business processes: includes measures focused on the question “What must we excel at?”

- Learning and growth: includes measures focused on the question “How can we continue to improve and create value?”

Managers generally use this tool to identify areas of the organization that need better alignment and control vis-à-vis the broader organizational vision and strategy. The balanced scorecard brings each of an organization’s moving parts into one view in order to improve synergy and continuity between functional areas. This video helps explain the Balance Score Card.

You can view the transcript for “Balanced Scorecard” (opens in new window).

Concept check

- Describe the control process.

- Why is the control process important to the success of the organization?

Media Attributions

- Private: 8.16.3